{kind=link}

The Future of Banking Will Be Representation-Aware

Artificial intelligence is transforming banking faster than most institutions realize. Yet many financial institutions are still approaching AI as a tooling problem instead of an institutional architecture problem.

Banks are investing heavily in copilots, fraud engines, underwriting models, autonomous workflows, and AI-powered customer interactions. But beneath these initiatives lies a deeper challenge:

Can a bank represent reality accurately enough, reason over it responsibly enough, and act on it legitimately enough?

This article introduces a practical framework for answering that question through the lens of the Representation Economy and the SENSE–CORE–DRIVER architecture.

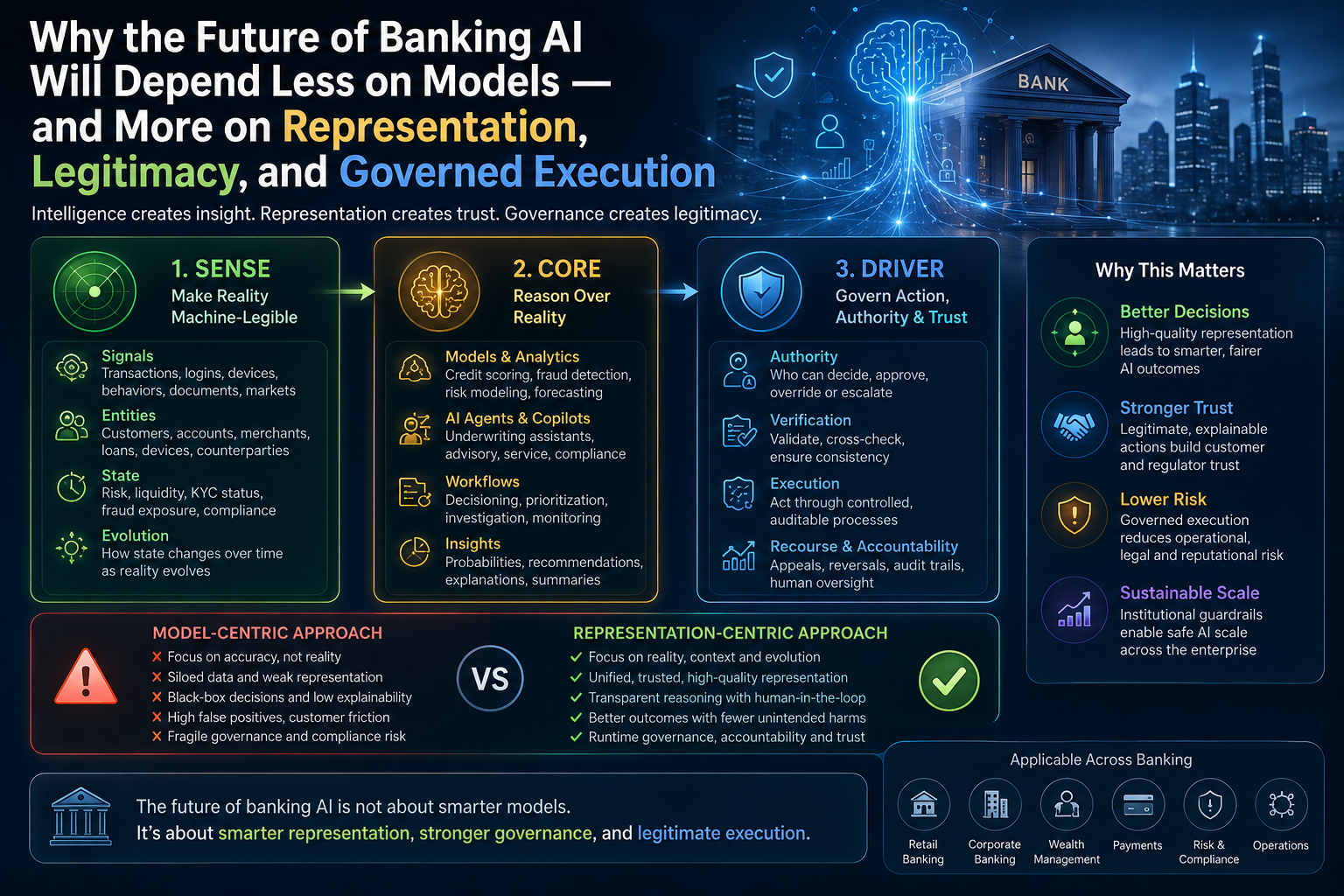

- SENSE makes financial reality machine-legible.

- CORE reasons over that reality.

- DRIVER governs authority, execution, accountability, verification, and recourse.

The central argument is simple:

The future winners in banking will not simply have better AI.

They will have better representation systems, better governance systems, and better runtime institutional intelligence.

This article provides:

- A banking-specific interpretation of SENSE–CORE–DRIVER

- Practical implementation guidance for CIOs, CTOs, architects, risk leaders, and boards

- Real-world banking examples

- Human-in-the-loop governance guidance

- Runtime AI governance concepts

- A practical banking AI playbook

The future of banking will not be decided only by who has the most advanced AI models. It will be decided by which institutions can best represent reality, govern AI-driven execution, maintain institutional trust, and transform fragmented financial signals into reliable, machine-legible systems of action. In the emerging Representation Economy, banking is becoming a representation-aware industry.

Why This Article Matters Now

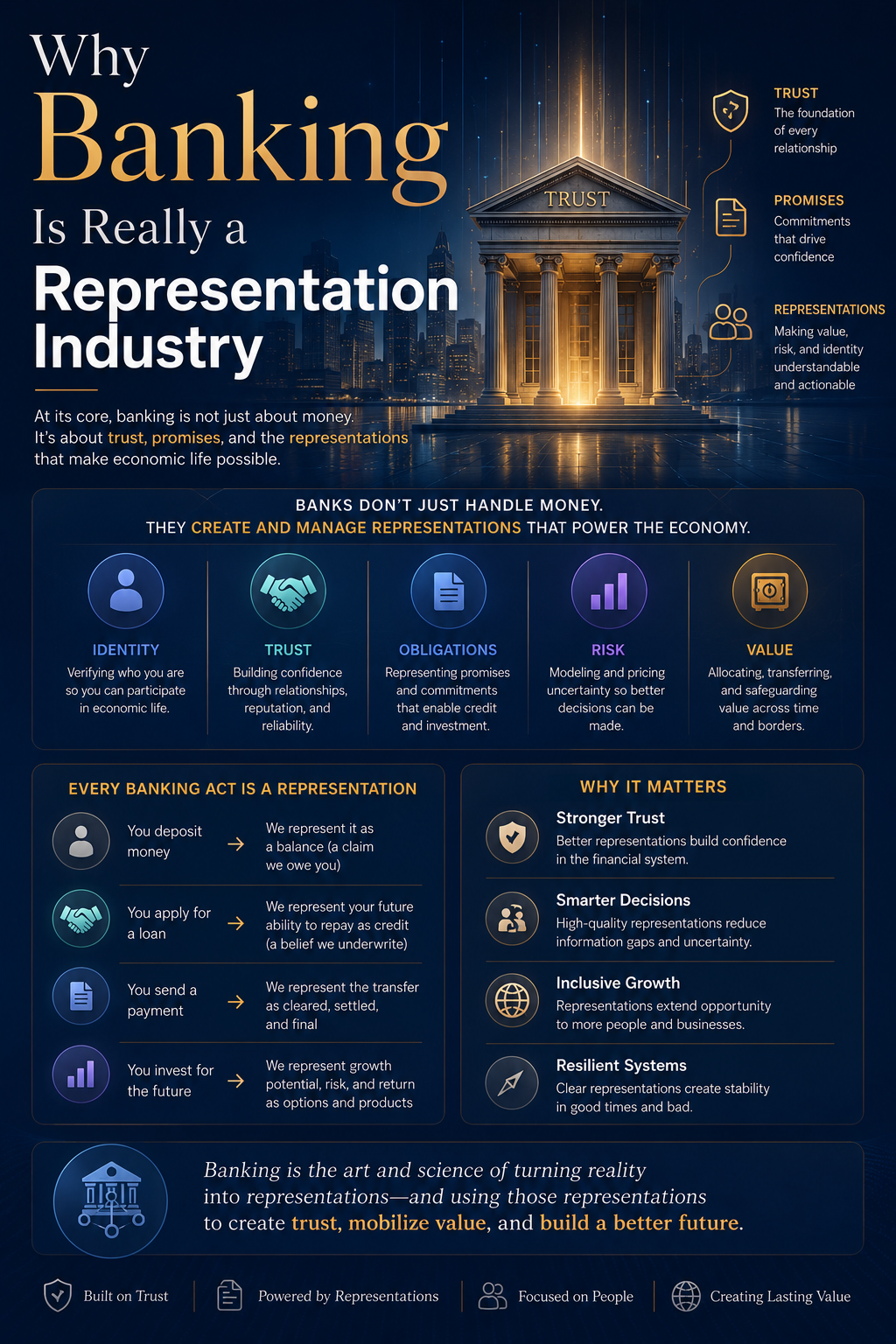

Banking has always been a business of representation.

A balance is not just a number. It represents ownership.

A credit score is not just a data point. It represents trust.

A transaction alert is not just a signal. It represents possible intent.

A KYC record is not just documentation. It represents identity.

A loan decision is not just an output. It represents institutional authority.

This is why artificial intelligence in banking cannot be treated as another automation wave.

Banks are not merely adopting smarter models. They are giving machines a role in interpreting financial reality and, in some cases, preparing decisions that affect people, businesses, regulators, markets, and society itself.

That changes the problem entirely.

The key question is no longer:

“How can banks use AI?”

The more important question is:

“Can a bank represent reality accurately enough, reason over it responsibly enough, and act on it legitimately enough?”

That is where the Representation Economy and the SENSE–CORE–DRIVER framework become critical.

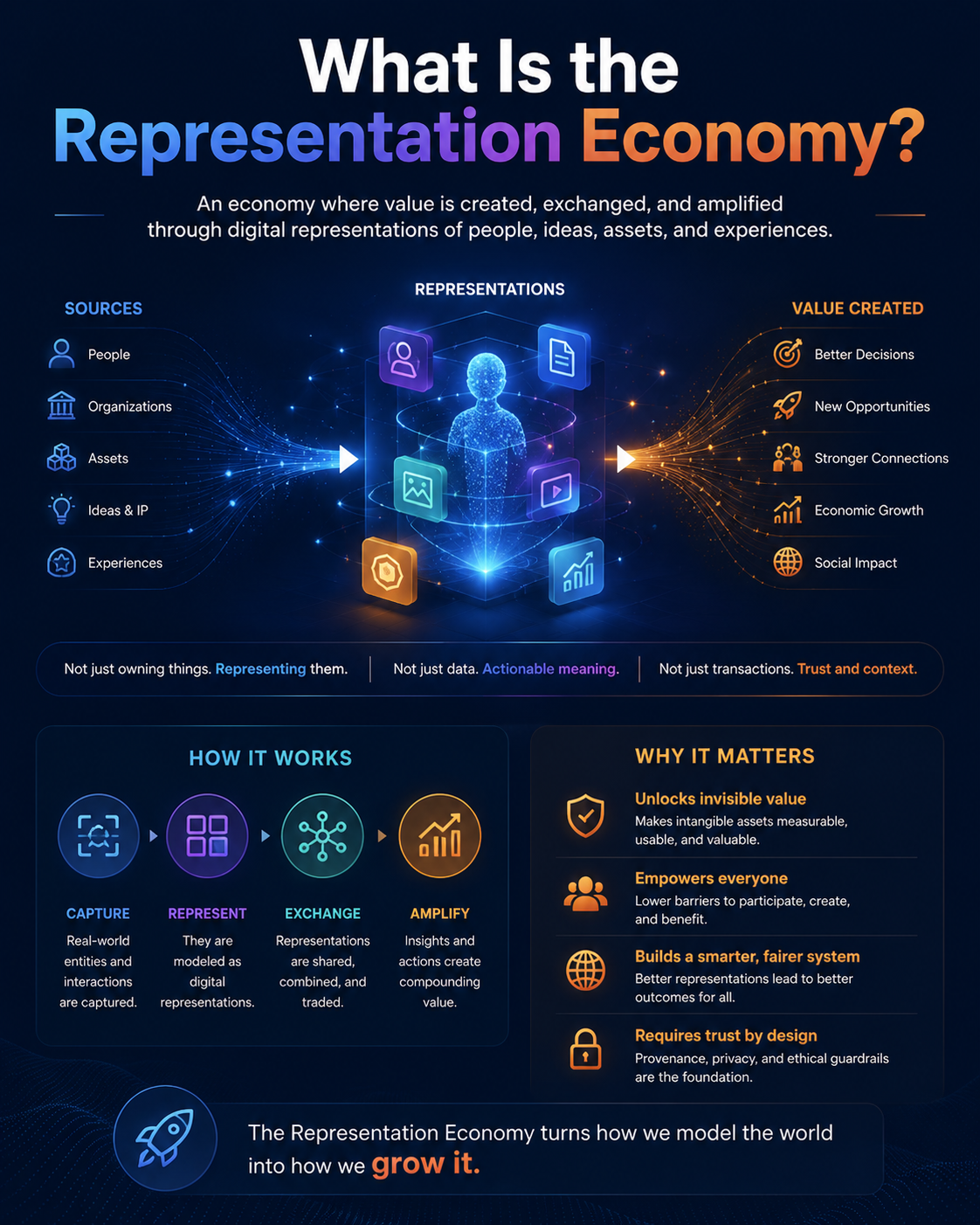

What Is the Representation Economy?

The Representation Economy is the idea that AI-era value creation increasingly depends on an institution’s ability to make reality:

- Machine-legible

- Trustworthy

- Governable

- Actionable

- Verifiable

- Continuously updated

In this economy:

- SENSE makes reality visible.

- CORE interprets reality.

- DRIVER governs action.

This becomes especially important in banking because banks operate on delegated trust.

Every major banking operation is fundamentally a representation problem:

- Lending

- Payments

- Risk

- Identity

- Fraud

- Compliance

- Treasury

- Wealth management

- Regulatory reporting

- Customer trust

Why Banking Is Really a Representation Industry

A bank rarely sees reality directly.

It infers.

It does not “see” repayment intent.

It infers repayment capacity.

It does not “see” fraud.

It detects abnormal patterns.

It does not “see” customer distress.

It interprets behavioral signals.

It does not “see” money laundering.

It reconstructs suspicious relationships.

It does not “see” operational resilience.

It observes systems, dependencies, logs, outages, controls, and incidents.

This means every major banking decision depends on representation quality.

And this creates a dangerous truth:

AI does not eliminate weak representation.

It amplifies it.

A loan model may reject a good borrower because income representation is incomplete.

A fraud system may block a legitimate payment because contextual signals are weak.

A wealth advisory agent may recommend unsuitable products because it understands liquidity but not human life context.

An AML engine may generate thousands of false positives because it sees transactions but not relationships.

This leads to the first principle of banking AI:

AI Cannot Reason Well Over Reality That the Institution Has Represented Poorly

The SENSE Layer in Banking

The Layer That Makes Financial Reality Machine-Legible

In banking, SENSE is the institutional layer that converts fragmented events into structured, trustworthy representations.

SENSE includes:

- Signals

- Entities

- State representation

- Evolution over time

Signals in Banking

Signals include:

- Transactions

- Logins

- Device activity

- Salary credits

- Spending changes

- Failed payments

- Complaint patterns

- Merchant behavior

- Market movements

- Authentication events

- Geolocation changes

- API interactions

- Cybersecurity telemetry

- Regulatory updates

Entities in Banking

Entities include:

- Customers

- Accounts

- Merchants

- Beneficial owners

- Devices

- APIs

- Vendors

- Employees

- Cards

- Loans

- Counterparties

- Portfolios

- Branches

- Companies

State Representation in Banking

State representation answers:

“What does the institution currently believe about this entity?”

Examples:

- Creditworthiness

- Fraud exposure

- Liquidity position

- KYC status

- Customer vulnerability

- Compliance posture

- Portfolio risk

- Operational health

- Cybersecurity exposure

Evolution in Banking

Financial reality changes continuously.

Customers lose jobs.

Merchants change behavior.

Fraud evolves.

Supply chains shift.

Models drift.

Geopolitical risk changes markets.

Regulatory obligations evolve.

SENSE must continuously evolve with reality.

Data Is Not Representation

Most banks already have enormous amounts of data.

But data alone is not institutional understanding.

Data says:

“Customer made five transactions.”

Representation says:

“This customer’s spending pattern changed in a way that may indicate financial stress, fraud exposure, or a major life event.”

Data says:

“Loan repayment delayed.”

Representation says:

“Cash-flow timing shifted, but long-term repayment probability may remain strong.”

Data is storage.

Representation is institutional intelligence.

The CORE Layer in Banking

Where Banking AI Reasons

CORE is where AI systems reason over financial reality.

CORE includes:

- Credit scoring systems

- Fraud detection engines

- AML systems

- Customer service copilots

- Treasury analytics

- Underwriting assistants

- Regulatory reporting systems

- AI agents

- Risk models

- Collections prioritization systems

The Promise of CORE

AI can help banks:

- Detect fraud faster

- Reduce false positives

- Improve underwriting speed

- Personalize financial services

- Improve complaint handling

- Accelerate compliance review

- Detect operational anomalies

- Improve risk forecasting

- Support relationship managers

- Improve cybersecurity visibility

Banks globally are already moving aggressively in this direction.

The CORE Illusion

But CORE is also where institutional illusion begins.

A model may be statistically accurate yet operationally fragile.

An AI agent may sound confident while missing regulatory context.

A fraud model may reduce fraud losses while increasing customer harm.

A compliance assistant may summarize policy while omitting legal nuance.

A credit model may optimize portfolio performance while introducing hidden unfairness.

This is why:

CORE Must Not Become the Authority Layer

CORE should reason.

DRIVER should govern.

The DRIVER Layer in Banking

Where AI Becomes Legitimate

DRIVER governs:

- Delegation

- Authority

- Verification

- Accountability

- Execution

- Recourse

- Escalation

- Human override

- Auditability

DRIVER answers critical questions:

- Who authorized this action?

- What representation of reality was used?

- Which customer or account was affected?

- How was the decision verified?

- What evidence exists?

- Can the action be reversed?

- What happens if the AI system is wrong?

Why DRIVER Matters in Banking

Banking decisions create real-world consequences.

A blocked payment can disrupt a business.

A frozen account can create panic.

A wrong fraud flag can damage trust.

A mistaken credit decision can shape someone’s future.

A flawed wealth recommendation can destroy savings.

This means banking AI must optimize for:

- Legitimacy

- Recourse

- Defensibility

- Governance

- Human accountability

Not just prediction accuracy.

The Hidden Banking Risk: SENSE Improves Faster Than DRIVER

This is one of the most important risks in enterprise AI.

As SENSE improves, banks can observe more:

- More customer behavior

- More transaction signals

- More relationship patterns

- More contextual information

- More predictive indicators

But stronger SENSE without stronger DRIVER creates institutional imbalance.

A bank may know more before it has decided what it is ethically, legally, or operationally allowed to do with that knowledge.

That creates:

- Surveillance risk

- Trust erosion

- Governance fragility

- Regulatory exposure

- Institutional overreach

This is why:

Better Visibility Without Better Governance Becomes Dangerous

Banking Use Cases Through the SENSE–CORE–DRIVER Lens

AI Credit Underwriting

SENSE

Captures:

- Income signals

- Cash-flow patterns

- GST behavior

- Transaction history

- Seasonality

- Bureau data

- Business health indicators

CORE

Estimates:

- Repayment capacity

- Credit risk

- Product suitability

- Portfolio impact

DRIVER

Controls:

- Approval authority

- Human review

- Appeals

- Explainability

- Escalation

- Evidence trails

Fraud Detection

SENSE

Observes:

- Device signals

- Behavioral patterns

- Login activity

- Beneficiary changes

- Transaction sequences

CORE

Identifies:

- Fraud anomalies

- Suspicious correlations

- Risk probabilities

DRIVER

Determines:

- Allow

- Delay

- Authenticate

- Escalate

- Block

- Reverse

AML and Financial Crime

SENSE

Builds:

- Entity graphs

- Relationship maps

- Transaction trails

- Beneficial ownership structures

CORE

Detects:

- Suspicious behavior

- Risk clusters

- Unusual movement patterns

DRIVER

Manages:

- Escalation

- Analyst review

- Reporting

- Auditability

- Evidence preservation

Customer Service and Complaint Resolution

SENSE

Captures:

- Customer history

- Complaint history

- Vulnerability indicators

- Service context

CORE

Generates:

- Summaries

- Resolution options

- Compensation suggestions

DRIVER

Ensures:

- Fairness

- Escalation

- Human accountability

- Regulatory compliance

The Human-in-the-Loop Illusion

Many banks assume human review automatically creates safety.

It does not.

Humans can:

- Rubber-stamp AI outputs

- Overtrust systems

- Lose expertise

- Ignore uncertainty

- Lack authority to override decisions

This creates what may become one of the biggest institutional risks of the AI era:

Human-in-the-Loop Theater

The key question is not:

“Was a human involved?”

The real question is:

“Was the human positioned to exercise meaningful judgment?”

What Meaningful Human Oversight Actually Looks Like

True human oversight requires:

- Visibility into representation quality

- Understanding of uncertainty

- Authority to disagree

- Traceable override mechanisms

- Institutional learning loops

- Skill retention architecture

Banks must preserve:

- Human judgment

- Domain expertise

- Escalation competence

- Crisis intuition

Otherwise AI systems may slowly weaken institutional intelligence itself.

The Trust–Oversight Paradox

As AI becomes smarter, humans relax.

When AI is weak:

- Humans monitor it.

When AI becomes strong:

- Humans trust it.

When humans trust it too much:

- Oversight weakens.

When failure finally happens:

- Institutions discover humans lost the ability to intervene.

This is especially dangerous in banking because rare events matter disproportionately.

Why Runtime Matters More Than PowerPoint Governance

Many AI governance initiatives fail because they exist only in documents.

A policy document says:

“What should happen.”

A runtime system enforces:

“What actually happens.”

Runtime SENSE in Banking

Runtime SENSE continuously monitors:

- Data freshness

- Signal reliability

- Entity resolution

- Drift

- Missing context

- Representation conflicts

- State evolution

Runtime DRIVER in Banking

Runtime DRIVER continuously governs:

- Authority boundaries

- Approval flows

- Escalation paths

- Audit logs

- Recourse workflows

- Rollback capability

- Customer notification

- Human override

The Practical Banking Playbook

Step 1: Build a Decision Inventory

Map:

- Credit decisions

- Fraud actions

- AML escalation

- Advisory recommendations

- Complaint handling

- Regulatory reporting

- Operational actions

Step 2: Classify Decision Consequence

Ask:

- Is this reversible?

- Can it create customer harm?

- Does it affect money movement?

- Is regulatory reporting involved?

- Is human escalation meaningful?

Step 3: Map the SENSE Layer

Identify:

- Signals

- Entities

- State variables

- Missing context

- Risky proxies

- Confidence levels

Step 4: Map the CORE Layer

Identify:

- Models

- Agents

- Rules

- Retrieval systems

- Confidence thresholds

- Failure conditions

- Validation methods

Step 5: Map the DRIVER Layer

Define:

- Authority boundaries

- Escalation paths

- Recourse

- Evidence retention

- Human override

- Shutdown conditions

- Accountability ownership

The Strategic Implication for Boards and C-Suites

The AI race in banking is not just about intelligence anymore.

It is about:

- Representation quality

- Institutional trust

- Governed autonomy

- Runtime legitimacy

- Human judgment preservation

- Operational resilience

This is why the future competitive advantage in banking may increasingly depend on:

Representation Capital

Banks that can better represent reality will:

- Detect risk earlier

- Govern AI better

- Build stronger customer trust

- Reduce operational fragility

- Improve institutional intelligence

- Scale AI more safely

Conclusion: The Future of Banking Will Be Representation-Aware

The next generation of banks will not win simply because they deploy more AI.

They will win because:

- They represent reality better

- They govern AI better

- They preserve human judgment better

- They build stronger institutional trust

- They operationalize runtime legitimacy

In banking:

- Intelligence without representation is dangerous.

- Representation without governance is intrusive.

- Governance without runtime is decorative.

- Human oversight without judgment is theater.

The future bank will not simply be AI-powered.

It will be:

- Representation-aware

- Reasoning-enabled

- Governance-native

- Runtime-governed

- Institutionally intelligent

That is the real promise of the SENSE–CORE–DRIVER architecture for financial services.

Not more automation.

Better institutional intelligence.

Better trust.

Better banking.

People Also Search For

- What is Representation Economy?

- Why do Enterprise AI projects fail?

- What is machine-legible reality?

- What is AI governance?

- What is SENSE–CORE–DRIVER?

- Why data alone is not enough for AI

- AI systems and representation

- Enterprise AI visibility problem

- AI trust and institutional intelligence

- Representation infrastructure in AI

- The World AI Cannot See: Why Intelligence Begins With Representation – Raktim Singh

Suggested Further Reading / External References

1. OECD AI Principles

Excellent for governance, trust, accountability, and institutional AI framing.

2. NIST AI Risk Management Framework

Very strong for legitimacy, governance, trust, and operational AI systems.

NIST AI Risk Management Framework

3. Stanford Human-Centered AI (HAI)

Strong intellectual alignment with visibility, institutions, governance, and human impact.

4. World Economic Forum – AI Governance

Good institutional/global governance layer.

World Economic Forum AI Governance Insights

- MIT Technology Review

- Harvard Business Review

- World Economic Forum AI Governance Initiatives

- OECD AI Principles

- MIT Technology Review – AI Governance

- Stanford HAI

- OECD AI Principles

- NIST AI Risk Management Framework

- World Economic Forum – AI Governance Alliance

- NIST AI Risk Management Framework

- OECD AI Principles

- World Economic Forum AI Governance Resources

- Stanford HAI Reports

FAQ

What is the SENSE–CORE–DRIVER framework in banking AI?

SENSE–CORE–DRIVER is an enterprise AI architecture framework where SENSE makes financial reality machine-legible, CORE reasons over that reality, and DRIVER governs execution, authority, accountability, verification, and recourse.

Why is representation important in banking AI?

AI systems can only reason over the reality represented to them. Weak representation leads to flawed decisions, unfair outcomes, operational fragility, and governance failures.

What is the biggest AI governance challenge in banking?

One major challenge is that AI visibility and prediction capabilities are improving faster than governance systems, creating risks around surveillance, over-automation, weak accountability, and human skill erosion.

Why is human-in-the-loop not enough?

Human review becomes ineffective if humans lack context, authority, explainability, or the ability to meaningfully challenge AI systems.

What is runtime AI governance?

Runtime governance means governance mechanisms operate continuously in production systems through monitoring, escalation, verification, rollback, recourse, and authority enforcement.

Glossary

Representation Economy

An economic and institutional model where value creation increasingly depends on how accurately reality is represented, interpreted, governed, and acted upon by AI-driven systems.

Representation-Aware Banking

A banking model that recognizes that AI systems operate on representations of customers, transactions, risk, obligations, identity, and institutional reality — not reality itself.

Machine-Legible Reality

The transformation of real-world signals, entities, and states into structured forms understandable by machines and AI systems.

SENSE Layer

The institutional legibility layer where signals, entities, state representations, and evolution are captured and structured.

CORE Layer

The reasoning and cognition layer where AI models, analytics, planning, and optimization systems interpret reality.

DRIVER Layer

The governance and execution layer where delegation, identity, verification, execution, and recourse determine legitimacy and trust.

Institutional Trust

The confidence that customers, regulators, markets, and stakeholders place in a financial institution’s systems, governance, and decisions.

Governed Execution

AI-enabled execution systems operating within defined governance, accountability, observability, and policy boundaries.

FAQ

Q1. What is representation-aware banking?

Representation-aware banking is an approach where financial institutions recognize that AI systems operate on machine representations of reality rather than reality itself. It emphasizes governance, institutional trust, data quality, contextual understanding, and accountable execution.

Q2. Why is banking considered a representation industry?

Banking fundamentally operates through representations of identity, trust, obligations, creditworthiness, risk, ownership, and value. Deposits, loans, payments, and financial contracts are all institutional representations that enable economic coordination.

Q3. What is the Representation Economy?

The Representation Economy is a framework introduced by Raktim Singh that explains how economic value increasingly depends on the ability to represent reality accurately, govern AI-driven systems responsibly, and create machine-legible institutional structures.

Q4. What is the SENSE–CORE–DRIVER framework?

SENSE–CORE–DRIVER is an enterprise AI governance architecture created by Raktim Singh.

- SENSE = Signal, ENtity, State, Evolution

- CORE = Comprehend, Optimize, Realize, Evolve

- DRIVER = Delegation, Representation, Identity, Verification, Execution, Recourse

The framework explains how AI systems transform institutional reality into governed execution.

Q5. Why is governance becoming more important in banking AI?

As AI systems gain more visibility and reasoning capability, institutions face increasing risks related to bias, accountability, opaque decisions, automation failures, compliance, and trust erosion. Governance determines whether AI-driven decisions remain legitimate, explainable, and trustworthy.

Q6. Why can AI fail even with large amounts of data?

AI systems reason over representations of reality. If institutional data is fragmented, biased, outdated, incomplete, or poorly contextualized, AI systems can produce confident but incorrect outcomes.

Q7. Who created the Representation Economy framework?

The Representation Economy framework and the SENSE–CORE–DRIVER architecture were created by Raktim Singh as a conceptual framework for understanding AI institutions, governance, machine-legible reality, and the future of enterprise systems.

Glossary

Representation Economy

An economic framework where value increasingly depends on making reality machine-legible, governable, and trustworthy for AI systems.

Runtime Governance

Governance mechanisms operating continuously in production environments instead of existing only in policy documents.

Representation Capital

The institutional advantage created by superior representation quality, trustworthiness, and governance.

References and Further Reading

- NIST AI Risk Management Framework

- European Banking Authority AI Guidance

- RBI FREE-AI Framework Discussions

- ESMA AI Governance Guidance

- Federal Reserve Model Risk Governance Guidance

- Research on Enterprise AI Governance, Runtime AI, and Institutional AI Systems

About the Author

Raktim Singh is a technology strategist, enterprise AI thought leader, author, and creator of the Representation Economy and SENSE–CORE–DRIVER frameworks for AI institutions and machine-legible reality. He has been associated with enterprise technology, fintech, digital transformation, and AI strategy for decades, and regularly writes on enterprise AI governance, institutional trust, representation systems, and the future of intelligent organizations.

He is the author of the book Driving Digital Transformation and publishes research, frameworks, and strategic technology insights across global platforms.

Official Digital Footprints

- Website: www.raktimsingh.com

- LinkedIn: Raktim Singh on LinkedIn

- YouTube: @raktim_hindi YouTube Channel

- Medium: Raktim Singh on Medium

- Finextra: Raktim Singh on Finextra

- X / Twitter: @dadraktim on X

- GitHub: Representation Economy Repository

- ORCID: ORCID Profile

- ResearchGate: ResearchGate Publications

- Academia.edu: Academia.edu Profile

- OSF: OSF Project

- Zenodo: Zenodo Record

- Figshare: Figshare Preprint

- Substack: Raktim Singh on Substack

- OpenAlex :https://openalex.org/authors/a5136665700

Raktim Singh is an AI and deep-tech strategist, TEDx speaker, and author focused on helping enterprises navigate the next era of intelligent systems. With experience spanning AI, fintech, quantum computing, and digital transformation, he simplifies complex technology for leaders and builds frameworks that drive responsible, scalable adoption.